If your mortgage is coming up for renewal, you’re not alone — millions of Canadians renew their mortgage every year. In 2026, the number is even higher due to the higher number of shorter term loans (2-4 years) taken over the last five years.

And here’s the mistake a lot of people make:

👉 They sign the renewal offer from their current lender without exploring their options.

It’s fast. It’s easy. I get that.

BUT, it could cost you thousands of dollars in unnecessary interest. We’ve had clients where their current lender has offered them rates that are over 0.75% higher than what we can offer.

Let’s break down what you actually need to consider before renewing.

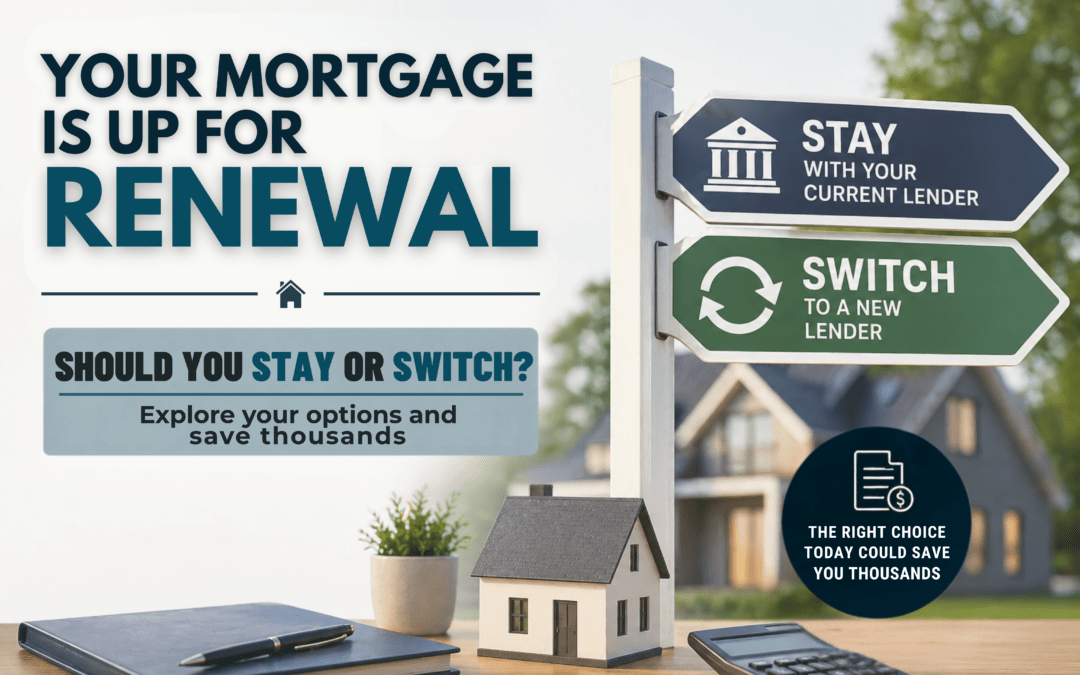

What Is a Mortgage Renewal?

When your mortgage term ends (typically after 1–5 years), your remaining balance doesn’t disappear — it needs to be renewed into a new term.

At that point, you have two options:

1. Stay with Your Current Lender

They’ll send you a renewal offer (usually 30–120 days before maturity).

Pros:

- Quick and convenient

- No income requalification (in most cases)

- No legal fees

Cons:

- Rates are often not their best offer

- Limited flexibility or negotiation

- You might miss better products elsewhere

2. Switch to a New Lender

You move your mortgage to a different lender offering better terms.

Pros:

- Potentially lower rate → saves money

- Access to better features (prepayment options, portability, etc.)

- Opportunity to restructure your mortgage

Cons:

- Requires income qualification (but sometimes not the stress test)

- Requires submitting income and financial documentation

- Legal/appraisal fees (sometimes covered by the new lender)

Why You Shouldn’t Auto-Renew

Your lender is counting on convenience.

Most renewal offers are not their most competitive rates — because they assume you won’t shop around.

Even a 0.50% difference in rate can mean:

- Thousands saved over your next term

- Lower monthly payments

- Faster equity growth

Here’s an example. A mortgage of $500,000, amortized over 25 years, will have approximately $12,000 in interest savings over a 5-year term with just a 0.5% rate reduction. That is not peanuts!

What Should You Compare Before Deciding?

A rate is important — but it’s not everything.

Here’s what a good broker will review with you:

✅ Interest Rate

Fixed vs variable — and what fits your risk tolerance

✅ Prepayment Privileges

Can you pay extra without penalties?

✅ Penalties

What happens if you break the mortgage early?

✅ Flexibility

Portability, blend-and-extend options, etc.

✅ Your Current Financial Situation

Has your income, debt, or goals changed?

✅ Your Future Plan

Are you planning any big life changes over the next 3-5 years?

When Switching Makes the Most Sense

Switching lenders is often a smart move if:

- Your renewal rate offered is higher than market rates

- Your financial situation has improved (better credit, higher income)

- You want to access equity or restructure debt

- Your current mortgage has restrictive terms

- You expect significant changes over the next 3-5 years

When Staying Might Be Better

In some cases, staying put is the right call:

- You won’t qualify with a new lender (income, credit changes)

- You prefer simplicity and speed

- Your lender offers a competitive renewal rate after negotiation

Pro Tip: Start Early

The best time to review your options is 6 months before your renewal date.

Why?

- You can potentially lock in a rate early

- You still have time to switch if needed

- It gives time to make changes if necessary

- You have time to setup a game plan!

How We Help

At renewal, you’re in a powerful position — you don’t have to stay where you are.

A good broker will help you:

- Compare multiple lenders (not just one bank)

- Negotiate better rates and terms

- Handle the paperwork if you decide to switch

- Make sure your mortgage still aligns with your goals

And the number one reason? A good broker will offer stress free, no pressure advice on what your existing lender is offering you. If your existing lender is offering you a really good deal, they will let you know that, and encourage you to sign the renewal paperwork.

Don’t Leave Money on the Table

Before you sign that renewal offer, it’s worth a quick review.

Even a short conversation could save you thousands.

👉 Reach out today for a free mortgage renewal review.

Recent Comments